When China began its Reform and Opening Up process in 1978, scholars debated whether it was a capitulation to Western capital and neoliberal globalization, or part of a long-game to develop China’s productive forces so as to create the material conditions for economic sovereignty and common prosperity. Only history could bear out the answers to these questions, and only now do we have the data and empirical tools to begin to answer them.

China’s reform-era trajectory, from the marketization process that began in 1978 to the ascension to the World Trade Organization in 2001, has been one of the most impactful entries of any major economy into the world market. China went from contributing less than 1% of world trade in 1978 to becoming the world’s largest trading country. China is now the top trading partner for 120 countries. Over half of the world’s busiest ports are in China.

However, this process of trade integration did not turn China into a mere appendage of the economies of the Global North. China retained sovereign control over natural monopolies while increasing domestic value addition and indigenous technological innovation. Today, China leads in 90% of critical technologies tracked by the Australian Strategic Policy Institute. It is the only country with a complete industrial ecosystem – producing products across every industrial subcategory defined by the United Nations.

We argue that China has both integrated into the global cycle of accumulation and ‘delinked’, borrowing the concept proposed by the Egyptian Marxist Samir Amin. When Amin proposed the concept of ‘delinking’ (déconnexion) as the strategic horizon for peripheral economies, he was careful to specify that delinking was not autarky; it was the subordination of external relations to the imperatives of internal accumulation.

This is precisely what China has achieved, but that outcome has been contingent on a very specific social settlement and institutional structure within China’s political economy. We call this ‘delinking with Chinese Characteristics’.

This article tracks China’s delinking using the Tricontinental: Institute for Social Research’s Structural Dependency Index (SDI). We then explore the social and institutional settlement that enabled this process by deploying the theory of the ‘constructive market’ by Chinese Marxist economists Meng Jie and Zhang Zibin, first translated into English in the international edition of Wenhua Zongheng: A Journal of Contemporary Chinese Thought.

China’s Structural Independence

The SDI is the first serious data-driven attempt to operationalize dependency theory. It draws on Brazilian Marxist economist Ruy Mauro Marini’s analysis of the capital-accumulation circuit (M–C…P…C’–M’) in dependent economies and decomposes it into six dimensions: financial (the monetary or M phase), technological and productive (the production or P phase), commercial and distributive (the realisation or M’ phase), and network dependency – which captures whether an economy occupies a central or appendage node in global value networks. Each dimension is normalized between 0 (maximum autonomy) and 1 (maximum dependency).

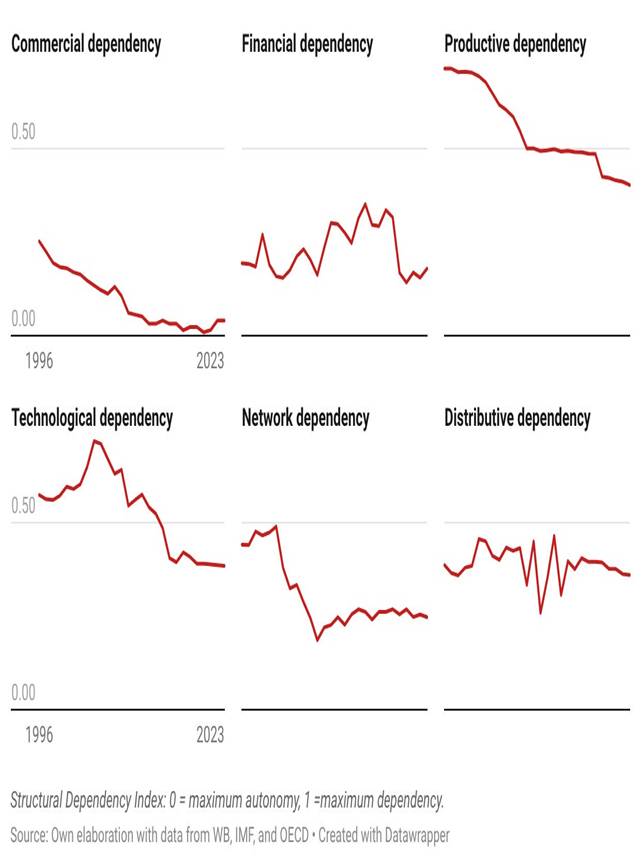

China’s trajectory on the panel is an outlier in the Global South. Its composite SDI fell from 0.6492 in 1996 to 0.3140 in 2022 – a 51% reduction, unmatched elsewhere in the sample.

Figure 1. China’s declining dependencies.

The reduction is sharpest in commercial dependency (0.253 → 0.041), which now sits near the measurement floor. China is the world’s dominant high-technology exporter, with mechanical and electrical products accounting for 58.6% of total exports by 2023.

Meanwhile, network dependency collapsed from 0.442 to 0.255 – this took place mainly after China’s accession to the World Trade Organization in 2001, which enabled China to become a major trade-network node rather than an appendage. By contrast, technological dependency rose between 2001 and 2004 as China deepened its integration into global value chains as an assembly hub. It then fell from 0.543 in 2012 to 0.386 in 2023 as the domestic value addition of production caught up through conscious industrial policies.

While productive dependency fell from 0.716 to 0.413, it remains higher than in South Korea, Japan, or Germany. Distributive dependency is the one dimension that has barely moved, from 0.387 in 1996 to 0.363 in 2022. These outliers reflect a historical condition: China’s gross fixed capital formation – consistently above 40% of GDP for three decades – was initially built on wage compression of migrant labor under the hukou system and on assembly positions with thin domestic value capture.

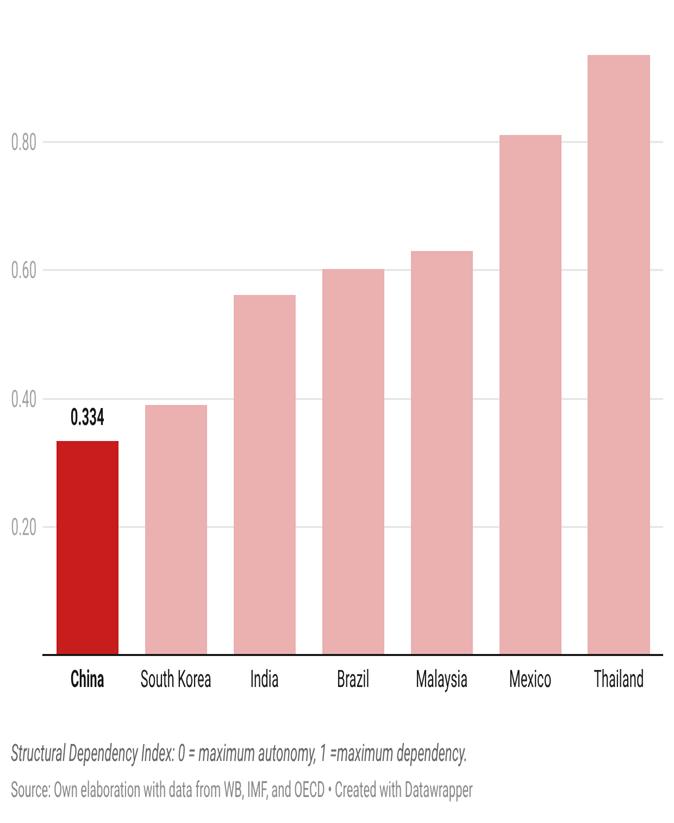

Figure 2. China’s delinking relative to the Global South (1996-2023)

The contrast with comparators in the Global South sharpens the picture. India’s SDI sits at 0.562 on a period average (1996–2023); its highest scores are in the technological and network categories, reflecting a services-led model in which India remains a node in technology chains rather than a technology generator.

South Korea’s period-average SDI is 0.390 despite OECD membership and the global presence of companies like Samsung and Hyundai – corporate scale does not necessarily translate into systemic centrality. South Korea’s network dependency remains among the highest in the panel because the country produces components for US-led semiconductor and electronics chains without controlling final-market channels.

What the SDI data shows is that China alone had a unique trajectory of simultaneous, multi-dimensional reduction of dependency at scale and speed. We argue that this result is not just a technical achievement but a result of how thoroughly the social, political, and institutional conditions for autonomous accumulation were assembled in China.

Constructing the Socialist Market

The SDI quantifies what changed. It does not, on its own face, explain how. Chinese Marxist economist Meng Jie has spent decades conducting primary research across China’s factories and state institutions to theorize its unique development trajectory. Together with Fudan University economist Zhang Zibin, his theory of the ‘constructive market’ is one of the most rigorous analyses of the architecture of China’s development.

Meng and Zhang’s distinctive theoretical step is to refuse both the Hayekian account of markets as spontaneously emergent and the Soviet-bloc resolution in which the state replaces the market. The ‘market’ in ‘constructive market’ is derived not from neoclassical price theory but from Volume II of Capital: the sphere of capital movement, characterized by the unity of production and exchange. The state does not regulate this market from the outside; it participates within it as architect and operator.

The state’s development strategy introduces a use-value goal into the market, which interacts with the exchange-value objectives pursued by enterprises, placing the former, as Meng and Zhang put it, ‘in a relatively dominant position’. What this means operationally is that the state actively constructs markets on both the supply and demand sides simultaneously, and only in strategic and foundational sectors.

The constructive market is not picking winners within an existing market nor subsidizing private investment after the fact. It is a system in which the state coordinates state-owned producers, targeted credit, technology-transfer requirements, procurement guarantees, consumer subsidies, and regulatory mandates asthe prior condition for the market’s existence.

China’s solar photovoltaics, electric vehicles, lithium-ion batteries, and high-speed railway are all results of this constructive market. They are markets that the state constructed before private capital could enter. More importantly, the constructive market prevents the escape of private capital into rentier and speculative ‘chokepoints’.

The Four Chokepoints

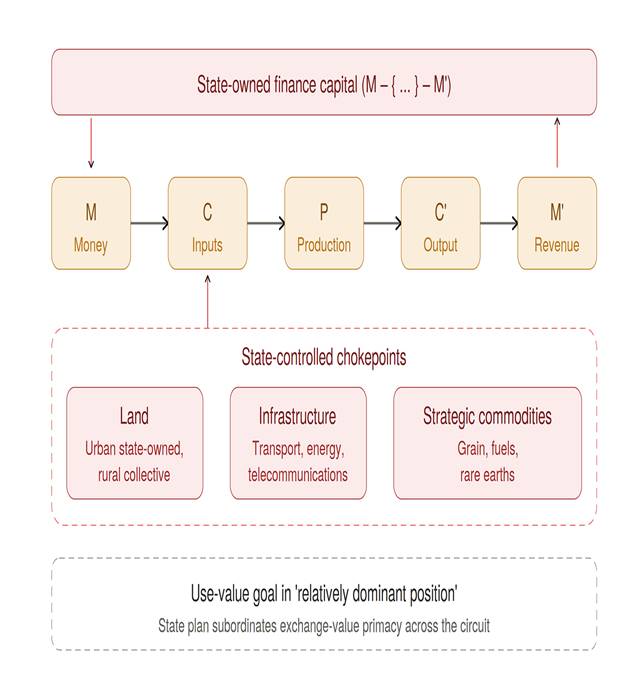

Meng and Zhang combine Marx’s circuit with German Marxist Rudolf Hilferding’s concept of finance capital to produce a formal expression of the state’s ownership and regulation of the financial sector: M – {M–C…P…C’–M’} – M’. State-owned financial capital enters productive capital with a primary aim other than profit. As they put it, ‘the primary goal of state-owned capital is to implement the objectives of socialist production and fulfill the tasks set by the national development plans and strategies’.

In this circuit, the state is able to direct M to the targeted sectors and collect M’ in a closed loop that denies private capital the ability to dominate the financial system. State-owned finance capital is the primary chokepoint that prevents private capital from dominating the accumulation process and crystallizing into monopolies – it also enables a long-term planning horizon.

Figure 3. Modified capital circuits with the state-owned finance capital

We add that this architecture is supplemented by at least three other institutional chokepoints that prevent capital from dominating the circuit of accumulation and locks it into competition within strategically defined sectors, thereby rapidly developing the productive forces. These three additional chokepoints are land, infrastructure, and strategic commodities.

In China, urban land is state-owned while rural land remains collectively owned at the village level. This arrangement places a hard cap on capital’s ability to flee competition in industrial sectors to amass wealth and collect rent.

Along with the land, the infrastructure built upon it – roads, railways, bridges, ports, power plants, telecommunication – remains under public control. This infrastructure is governed as a public good, helping keep production and transaction costs down, supporting the real economy, and once again denying private capital a natural monopoly from which to extract rents.

Finally, strategic commodities – from food grains to hydrocarbons and rare earth minerals – are predominantly produced, processed, and traded by state-owned entities. This is supplemented by a complex state-owned system of strategic reserves to stabilize prices during shortages and external shocks. Like other chokepoints, this prevents private capital from entering into an arena where it is incentivized to speculate and raise costs at the expense of downstream production.

The four chokepoints of finance, land, infrastructure, and strategic commodities discipline capital’s exchange-value orientation to the use values set by the state. This is what distinguishes the architecture from ‘developmental’ and ‘entrepreneurial’ states, where public investment generates private returns while equity stakes and operational control are absent. In the Chinese arrangement, state-owned finance capital retains both. The M – {M–C…P…C’–M’} – M’ circuit begins and ends with public capital.

Chinese Delinking in Action

The US-imposed trade and tech war on China provides a natural experiment to evaluate how China’s constructive market responds to external pressure. In one of our previous newsletters, we highlighted how the trade war of Trump 2.0 has created a tendency towards re-compradorisation in the Global South. We argued that the SDI data for countries such as South Korea, Malaysia, and India essentially foretold the capitulation of their elites in response to the threat posed by access to the US market and technology. But this was not the case with China.

Unlike its regional peers, China has not only withstood US tariffs and export controls but has actively built alternative markets and domestic technological capabilities in their place. To understand why this is significant, it helps to trace the specific pressure China was placed under – and what it produced in response.

The pressure began in earnest in October 2022, when the administration of US President Joseph Biden launched what former National Security Advisor Jake Sullivan described as a ‘small yard, high fence’ semiconductor siege: targeted controls on advanced chips, lithography machines, and chip-design software. Over the following three years, the restrictions expanded steadily, eventually placing more than 700 Chinese firms under the extraterritorial reach of the Foreign Direct Product Rule – meaning any product made anywhere in the world using US technology could be blocked from reaching Chinese buyers.

China responded through coordinated mobilization of its constructive market. State-owned finance capital scaled the China Integrated Circuit Industry Investment Fund by $47.5 billion in May 2024, channeling capital into the domestic semiconductor supply chain. Local experimentation across firms such as Semiconductor Manufacturing International Corporation, Naura, Advanced Micro-Fabrication Equipment, and SiCarrier began producing domestic substitutes for the equipment that Chinese foundries could no longer import.

The results have exceeded most outside expectations. In August 2023, Huawei released a smartphone containing a 7nm processor manufactured by SMIC – a feat widely considered improbable, if not impossible, given the restrictions in place. By late 2024, China’s mature-node chip capacity had reached 31% of the global total. Then, in December 2025, Reuters confirmed that a domestically assembled extreme ultraviolet (EUV) lithography prototype was operational and undergoing testing, with functional chip production targeted for 2028.

This is delinking in the sense that Amin meant it: not borders closed against trade, but the institutional capacity to reproduce – at scale and on demand – the technology that the imperial core treats as a monopoly.

Development Praxis for the Global South

The SDI measures delinking from the outside. The constructive market explains it from the inside. Two methods examining the same phenomenon, converging on a single proposition: sovereign industrialization based on autonomous accumulation is, in fact, possible.

Dependency falls when society retains structural authority over capital and subordinates the demands of external extraction to internal accumulation. Where these conditions hold, the SDI falls across all six dimensions at once, as in China. Where any are absent, dependency reproduces itself regardless of who is formally in power. India’s services-led integration and South Korea’s component-supplier integration are the comparator cases.

However, a precondition of China’s delinking and constructive market was the process set in motion in 1949 – the dismantling of private, rent-seeking, and comprador forces. This political process is the origin of the chokepoint architecture mentioned earlier. Where that dismantling has not happened – which is to say, across most of Latin America, Africa, and parts of Asia – the chokepoints are captured by comprador fractions of the domestic bourgeoisie and converted into instruments of dependency reproduction.

The chokepoints are not technologies that can be lifted out and installed. They are crystallised outcomes of a class struggle that elsewhere remains pending. Any account that reads the Chinese architecture without reading the political condition for its possibility repeats the central error of forty years of developmental-state literature.

The constructive market and chokepoint architecture replaces the question ‘what should (or shouldn’t) be nationalized?’ with a sharper one: where in the accumulation circuit does the surplus get captured, and how can the state retain authority over that node?

The IMF and World Bank conditionality across the Global South militate against the kinds of policies and institutional structures described above. Privatization and austerity have stripped states of anti-monopoly disciplinary capacity. However, the partial retreat from capital-account liberalization across the Global South – from Argentina’s currency controls (2011–2025) to Russia’s post-2022 emergency measures to the broader BRICS-plus reflection on alternatives to dollar clearing – is the most consequential institutional reversal of the neoliberal period. Whether that reversal becomes structural or remains episodic is the question on which the rest hinges.

Capital-account governance is the precondition for the other three chokepoints. Without sovereign authority over cross-border financial flows, the surplus that the chokepoints capture leaks out through portfolio repatriation, transfer pricing, and offshore reinvestment, and disciplinary architectures lose their bite, because monopoly capital can always exit. China’s SOEs would not have survived the 1997 restructuring had the renminbi been freely convertible.

Of course, we do not say that the ‘Chinese model’ has solved development for the Global South. Or that there is an easily replicable and transferable ‘Beijing Consensus’. During China’s reform process, Deng Xiaoping popularised the Chinese idiom ‘crossing the river by feeling the stones’. Our proposition is that feeling the stones that China crossed to get where it is today can provide us with the contours of what is to be done in other contexts.

Shiran Illanperuma is a researcher at Tricontinental: Institute for Social Research and a co-editor of the international edition of Wenhua Zongheng: A Journal of Contemporary Chinese Thought. He is a visiting lecturer at the Bandaranaike Center for International Studies.